.png)

A conversation between David Phillips, CEO of Fondo, and Jake Wedig, Director of Tax at Fondo, about the recent tax legislation changes affecting startups and business owners.

A conversation between David Phillips, CEO of Fondo, and Jake Wedig, Director of Tax at Fondo, about the recent tax legislation changes affecting startups and business owners.

Want to chat with a Fonda CPA? Get in touch!

Q: What makes working in tax exciting, especially for startups?

Jake: What I love about tax is that when you think about the two main paths from accounting to audit and tax, I've always felt that tax allows me to actually save clients money and make a real difference for their business. You feel really helpful with that planning and strategy aspect. While audit is important too, it's essentially a required expense just to stay compliant. With tax, I'm actively working toward my clients' interests through tax resolution and planning. And it's a particularly exciting time right now with this new tax bill that just passed.

Get more info on how you can benefit from the new tax bill: https://section174.tryfondo.com/

Q: Tell us about this "big beautiful bill" that just became law.

Jake: This bill was signed into law on Friday, July 4th, and it's over 900 pages long. There's a lot in it. Some good things, interesting changes, some cuts, but I want to focus on what's most important for our clients on the business side, particularly startups.

The biggest change I'm excited about relates to R&D credits. These are incentives where if you develop something in the US, thinking about wages, contractor costs, hosting costs, whatever you need to develop a new product or service, there can be incentives from the IRS to essentially get you cash back through tax credits.

Q: Can you explain what R&D means for startups specifically and how will it save money?

David: This is really important because R&D for startups is essentially all your payroll headcount for product and engineering. We're talking about designers, developers, founders, the people building the product and creating something new. There are two main buckets: Section 41, which relates to the R&D tax credit and covers payroll, and Section 174, which includes payroll plus health benefits, office space allocated to engineers, health insurance, and all the expenses around R&D.

Q: What was the problem with Section 174 that hurt startups?

Jake: Back in 2017 with the Tax Cuts and Jobs Act, there was a sunset provision that took effect in 2022. Without getting too deep into the mechanics, they had to think through budget implications and ensure they weren't overspending or under-collecting revenue. They created a provision where any business with R&D activity had to add back those expenses and amortize them over either five years if domestic, or 15 years, if international.

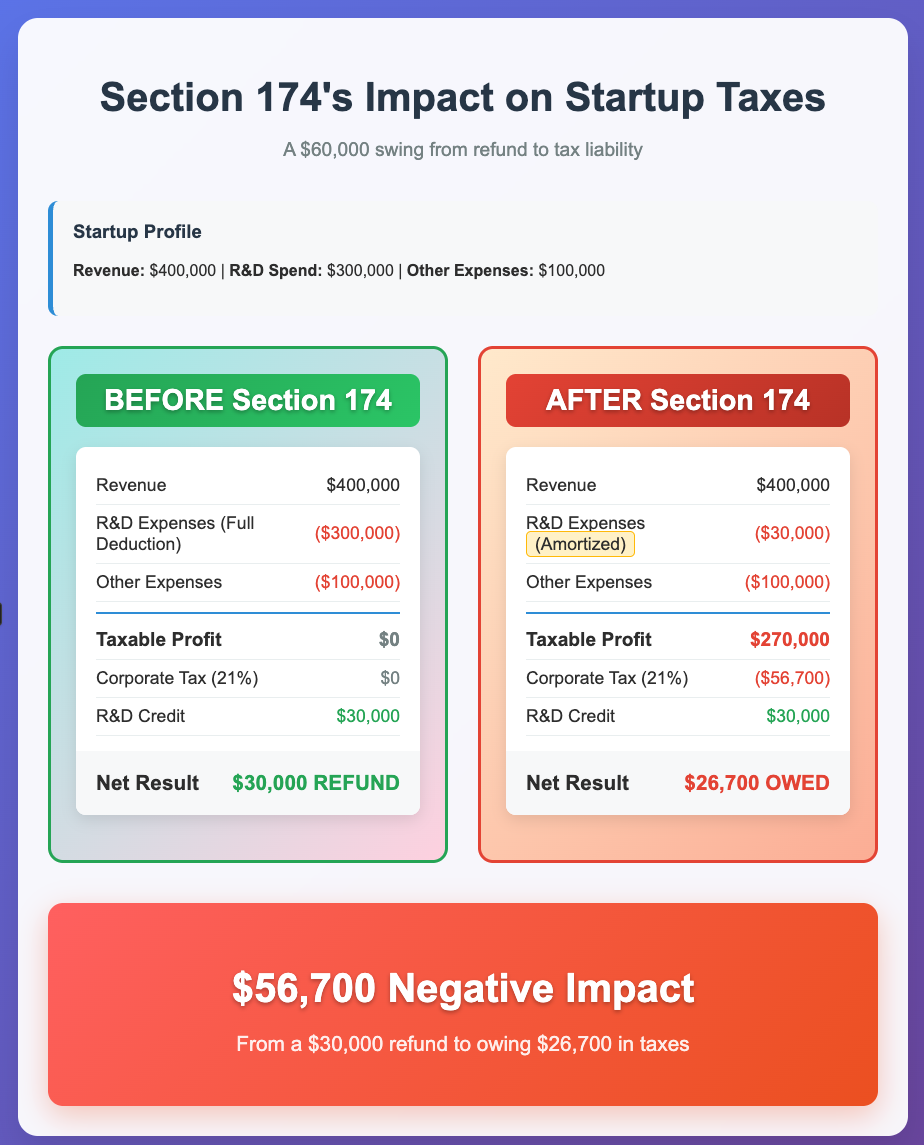

David: Here's a concrete example of how this hurts startups: Let's say you're a startup making $400,000 in revenue with $300,000 in R&D spend and $100,000 in other expenses. Normally, you'd have zero profit and no taxes owed, plus you'd get about $30,000 back as an R&D credit.

But after Section 174 took effect, instead of deducting the full $300,000 in R&D expenses, you could only take about $30,000 in the first year due to the amortization rules. So now you had $400,000 in revenue minus $130,000 in total deductions, leaving you with $270,000 in taxable profit. At the 21% corporate tax rate, you'd owe about $56,000 in taxes. After the R&D credit offset, you'd still owe around $30,000. So you went from getting $30,000 back to owing $30,000—a $60,000 swing against you.

Q: How does the new bill fix this problem?

Jake: Starting with the 2025 tax year, Section 174 domestic capitalization requirements are eliminated. This means you can go back to taking full deductions for R&D expenses, returning to the previous situation where you'd owe no taxes and get the full cash credit amount.

We can help you do this for your business at Fondo. Get in touch and see how: https://section174.tryfondo.com/

Q: Should startups amend their prior year returns?

Jake: It depends on your specific situation. Amending only makes sense if you were pushed into a taxable position because of Section 174. There's also a small business exception, I believe it's around $31 million in gross receipts, that triggers the ability to amend.

For many clients, there's going to be an opportunity to do "catch-up deductions" for any amortization that still hasn't been taken, which might be the best opportunity rather than amending.

Q: How do these catch-up deductions work compared to amending?

Jake: This is where it gets interesting from a planning perspective. If you amend your returns, you'll have a larger net operating loss (NOL) to carry forward, but you can only use 80% of that NOL in the current year. However, with catch-up deductions, you can treat those unamortized expenses as current-year expenses and utilize 100% of them.

David: So the key analysis is: Do you increase your NOL for prior years, or do you take those unamortized deductions fully this year? For example, if you're going to be profitable this year and have catch-up deductions available, you might be able to offset more of your current profit than you could with the 80% NOL limitation.

Q: What about pre-revenue startups? How were they affected?

Jake: If you're pre-revenue with no income to tax, your R&D credit becomes a payroll tax credit, essentially cash back. This isn't changing with the new rules. The biggest impact for pre-revenue companies is that they'll increase their NOL if they amend, but they'll be able to accelerate those deductions to 2025 and still get the NOL they expected, just one year later.

David: Here's an example: If you were a pre-revenue startup that spent $1 million on R&D last year, you got a $100,000 R&D credit, but because of Section 174, you only got a $100,000 NOL instead of the full $1 million. You're missing out on $900,000 in NOL carry-forward. The question is whether it's better to amend and get that $900,000 NOL (but only use 80% of it) or take the catch-up deductions this year at 100%.

Q: Does this change affect international R&D differently?

Jake: Yes, this is important to note. The new law only impacts domestic research. International R&D still has the 15-year amortization requirement. This creates a significant incentive to keep R&D domestic.

David: The math is striking. If you have $1 million in revenue and $1 million in domestic R&D expenses, you'd have zero profit and get a $100,000 R&D credit. But if that $1 million is spent on international talent, you'd have about $967,000 in taxable profit (since you can only deduct about $33,000 in the first year of the 15-year amortization), resulting in about $200,000 in taxes owed. So your effective cost for hiring domestically is $900,000, while hiring internationally effectively costs $1.2 million.

Q: What should startups do right now?

Jake: The first step is reaching out to your tax advisor, or get in touch with our expert team at Fondo, to understand your last three years of activity. You need to understand: Have you been paying taxes due to Section 174? Have you been receiving the R&D credit you expected? If you've been getting your R&D credit properly through payroll tax credits as an early-stage startup, you might want to stay the course because amending could create more administrative costs than benefits.

You also want to think about your cash flow and goals for next year. Are you going to be profitable? Would it be more helpful to capture more deductions next year than to amend and have an NOL that's capped at 80%?

Q: What other changes should startups know about?

Jake: Bonus depreciation is back at 100%. This means if you're spending money on equipment, instead of depreciating it over its useful life (typically 3, 5, or 7 years), you can take 100% of that depreciation in the current year. So if you buy a $10,000 computer, you can depreciate the full $10,000 this year instead of spreading it over five years.

David: That's a significant cash flow benefit. For every $100,000 in depreciable assets you purchase, you're potentially saving about $21,000 in taxes in that first year at the 21% corporate rate.

Q: How does this relate to Section 179 depreciation?

Jake: Section 179 was also expanded—the deduction cap increased from $1 million to $2.5 million. However, Section 179 has a limitation: you can't go into a net operating loss with it. Bonus depreciation, on the other hand, can create or increase an NOL, which makes it more impactful for startups that are pre-revenue or spending heavily.

Q: Tell us about the QSBS changes.

Jake: Qualified Small Business Stock (QSBS) got a major upgrade. Previously, if you were a startup founder and held your initial stock for five years, you could exclude up to $10 million in capital gains when you sold. Now, that exclusion has been increased to $15 million.

Even better, there's now a tiered exclusion system. You no longer have to wait the full five years. At three years, you get a 50% exclusion; at four years, you get 75%; and at five years, you get the full 100% exclusion on up to $15 million.

David: This is huge for founders. If you sell your company and personally receive $15 million in proceeds, instead of paying about $3.57 million in federal capital gains taxes (at a combined rate of 23.8% — 20% capital gains plus 3.8% NIIT), you'd pay nothing on the federal level if you qualify for QSBS.

Q: Are there any timing considerations for QSBS?

Jake: Yes, this is crucial and this only applies to stock issued after the bill's enactment. So if you're thinking about incorporating your company, now is the time to start that five-year clock.

David: If you incorporate as a Delaware C Corp now and sell in five years, you'll get the full $15 million tax-free on the federal level. That's a potential savings of over $3.57 million in federal taxes alone.

Q: What's your advice for navigating these changes?

Jake: There's a lot of complexity here, and the guidance is still evolving. You really want a tax advisor who can be in the weeds with you on this process because there's significant money to be saved from a tax and cash flow perspective by setting things up correctly.

Every situation is different. You might have been pre-revenue last year but could be generating significant revenue this year. The analysis of whether to amend, take catch-up deductions, or just move forward depends on your specific circumstances.

David: At Fondo, we're focused on helping our clients navigate these changes to maximize their tax credits, minimize their taxes owed, and ensure compliance. If you're already a Fondo customer, we'll walk you through this and make sure you're getting your maximum benefit. If you're not a customer yet, we'd be happy to help you understand how these new changes affect your specific situation.

Q: Any final thoughts?

Jake: This is a really exciting time for startups from a tax perspective. We're seeing incentives that truly support innovation and domestic development. But don't try to navigate this alone, there are significant opportunities to save money, but also potential pitfalls if you don't understand the rules.

The key is to be proactive. Talk to your tax advisor now, understand your situation over the past three years, and develop a strategy that maximizes your benefits going forward. With proper planning, these changes can result in substantial cash savings that can be reinvested in growing your business.

David: Taxes exist for two main reasons: to generate revenue and to provide incentives. These changes clearly show the government wants to incentivize domestic R&D and startup formation. As a founder myself, I recommend all businesses take advantage of these incentives since they're specifically designed to help businesses like yours succeed.

For more information about how these tax changes might affect your startup, consider consulting with a qualified tax professional who specializes in working with startups and understands the complexities of R&D credits, depreciation rules, and QSBS planning.

Simplify Startup Finances Today

Take the stress out of bookkeeping, taxes, and tax credits with Fondo’s all-in-one accounting platform built for startups. Start saving time and money with our expert-backed solutions.

Get Started

.png)