📚 Get back to building, not balancing books

Get Started We’ve helped hundreds of international founders since we launched our global tax product. Here is a comprehensive guide that answers all of the most common questions international founders have about corporate US taxes for startups.

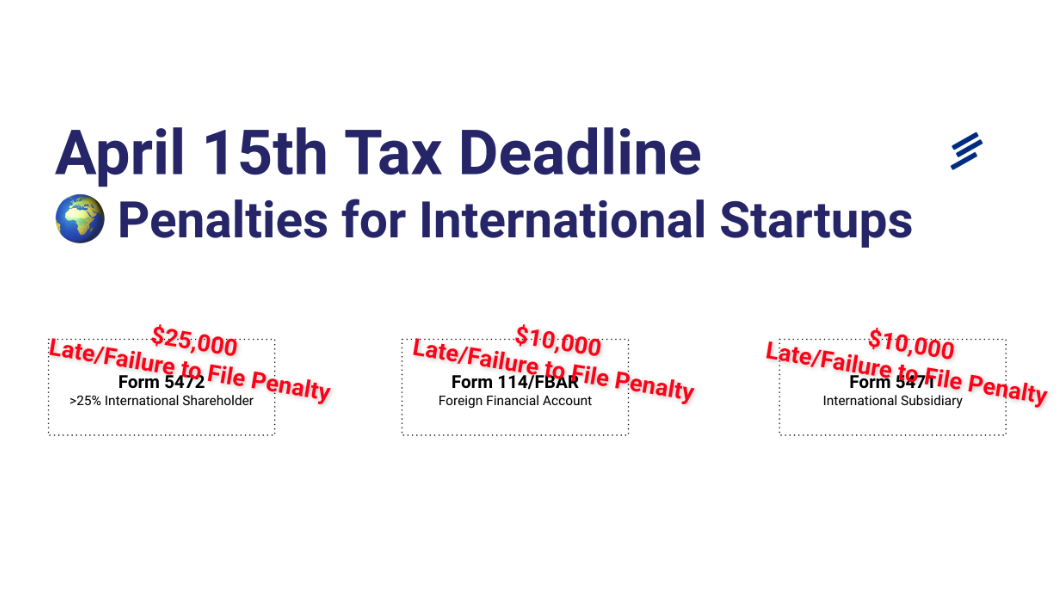

URGENT: If you have an international shareholder who owns 25%+, have corporate bank accounts located outside of the US with $10,000+, or have a subsidiary located outside of the US, you may face $10,000+ in tax penalties if you do not file a tax extension or file your taxes on time (due on Monday April 15th).

We highly recommend you file an extension. We’d love to help you if you have not filed yet — Fondo can file your Federal Tax Extension to avoid these penalties for when you sign up by Friday at 6pm PST, we will also provide a personalized Startup Tax Plan that outlines your tax obligations (it’s only $1): tryfondo.com/1

Each year, beginning with the year of incorporation, startups need to file & pay:

Once your startup is incorporated as a Delaware C Corporation, you will need to file corporate taxes — even if you have no financial activity during the year. That means that you are required to file corporate taxes for every year your company exists, beginning with the year of incorporation. If your Delaware C Corp has overseas any international relationships (founders, banks, subsidiaries) you will be required to file international forms in addition to all standard US corporate tax items.

The good news is that you can automate all of this for a small cost by using Fondo, we can make sure you get an ROI on this by helping you get cash back from the IRS (the average startup gets $21k back).

All Delaware C Corporations are required to pay and file Delaware Franchise Tax whether or not the company has any income, expenses, or financial activity.

All U.S. Corporations are required to file:

(1) Federal Corporate Income Tax Return (form 1120) whether or not the company has any income, expenses, or financial activity.

If foreign shareholder with 25%+ ownership:

(2) Form 5472

If foreign bank account with a balance of $10k+ during the year

(3) Report of Foreign Bank and Financial Accounts (FBAR) - FinCEN Form 114

If foreign subsidiary:

(4) Form 5471

If you are “doing business” in any states (i.e. have W-2 employees — not 1099 contractors or consultants, an office, fixed assets, or sales — typical state-specified threshold is $100,000) you will have to file and pay State Corporate Income Tax in that state.

Delaware looks at total share counts and gross assets (i.e. Cash, Treasury Accounts & other investments, Fixed Assets like machinery & equipment, Crypto, Inventory, Investments or Loans to Foreign or Domestic Subsidiaries) to determine the amount of Franchise Tax you owe. There are two methods to calculate the total Delaware Franchise Tax: the Authorized Shares Method and Assumed Par Value Capital Method. Delaware gives startups the flexibility to use the method that results in the lesser tax -- in most cases this will be Assumed Par Value Capital Method. The minimum due is $450.00 (Guide to Delaware Franchise Tax for Startups)

The current U.S. corporate tax rate is 21%. The corporate tax rate applies to your startup’s taxable income, which is essentially your revenue minus expenses. If your startups doesn’t have taxable income (i.e. profits), you will owe $0.

If you have $200,000 in taxable income you will owe $42,000 — however if you work with Fondo we can help make this $0 or even help you get a refund from the IRS (average startup’s we help owe $0 and will get $21,000 back from the IRS).

Most states set a corporate tax rate in addition to the U.S. rate. State corporate income tax rates range from 0% – 9.99%. But, not all states have a corporate tax rate.

The following states do not have a state corporate tax rate: Nevada, Ohio, South Dakota, Texas, Washington, Wyoming.

Nevada, Ohio, Texas, and Washington have gross receipts tax on corporations instead of corporate taxes. A gross receipts tax is a tax on a startup’s gross receipts, which includes the startups’s total revenue WITHOUT deductions (i.e. operating expenses).

South Dakota and Wyoming do not have state corporate income taxes at all.

Keep in mind that some states have both corporate income tax and gross receipts tax.

Some states apply a flat tax to all corporations while others use brackets. Some states have a minimum Franchise Tax due (i.e. California has a minimum Franchise Tax of $800). The states with brackets apply tax rates based on the corporation’s taxable income — Alabama: 6.5%; Alaska: 0% – 9.4%; Arizona: 4.9%; Arkansas: 1% – 5.9%; California: 8.84%; Colorado: 4.63%; Connecticut: 7.5%; D.C.: 8.25%; Delaware: 8.7%; Florida: 5.5%; Georgia: 5.75%; Hawaii: 4.4% – 6.4%; Idaho: 6.5%; Illinois: 7% (+2.5% replacement tax); Indiana: 4.9%; Iowa: 5.5% – 9.8%; Kansas: 4% (+ a 3% surtax on net income in excess of $50,000); Kentucky: 4% – 6%; Louisiana: 3.5% – 7.5%; Maine: 3.5% – 8.93%; Maryland: 8.25%; Massachusetts: 8%; Michigan: 6%; Minnesota: 9.8%; Mississippi: 3% – 5%; Missouri: 4%; Montana: 6.75%; Nebraska: 5.58% (+7.50% on taxable income of the excess over $100,000); Nevada: N/A; New Hampshire: 7.7%; New Jersey: 6.5% – 9%; New Mexico: 4.8% (+5.9% of excess over $500,000); New York: 6.5% – 7.25%; North Carolina: 2.5%; North Dakota: 1.41% – 2.9%; Ohio: N/A; Oklahoma: 4%; Oregon: 6.6% – 7.6%; Pennsylvania: 9.99%; Rhode Island: 7%; South Carolina: 5%; South Dakota: N/A; Tennessee: 6.5%. Texas: N/A; Utah: 5%; Vermont: 6% – 8.5%; Virginia: 6%; Washington: N/A; West Virginia: 6.5%; Wisconsin: 7.9%; Wyoming: N/A.

If you have engineers or founders on US payroll, the government offers many Tax Credits to help startups offset research and development costs, hiring employees, and more. Most startups don't know that certain credits offer direct cash back from the IRS — even if the company does not have any profits or owe any income taxes. The average startup we help gets $21,000 back from the IRS. This guide discusses the most beneficial tax credits for startups, how to qualify, and how to claim them. To see if you qualify and how much you can get back see here.

Your Delaware Annual Franchise Tax Report and payment is due by March 1.

Your U.S. Corporate Income Tax Return (form 1120) is due by April 15. You can file an extension which will extend your deadline by 6 months — to October 15. However, you will need to pay any taxes owed with your extension. In order to qualify for R&D Tax Credits (payroll election), you cannot miss this deadline.

Your State Corporate Income Tax Return(s) are typically due by April 15. You can file an extension which will extend your deadline by 6 months — to October 15

However, you will need to pay any taxes owed with your extension.

The penalty for paying and filing a late Delaware Annual Franchise Tax Report is $200 + 1.5% per month on your outstanding balance due.

(1) Federal Corporate Income Tax Return (form 1120) whether or not the company has any income, expenses, or financial activity: 5% of the unpaid tax for each month or part of a month the return is late, up to a maximum of 25% of the unpaid tax.

If foreign shareholder with 25%+ ownership:

(2) Form 5472 - $25,000 per shareholder

If foreign bank account with a balance of $10k+ during the year

(3) Report of Foreign Bank and Financial Accounts (FBAR) - FinCEN Form 114 - $10,000 per bank account

If foreign subsidiary:

(4) Form 5471 - $10,000 per subsidiary

Varies by state, typically up to 5% of the unpaid tax for each month or part of a month the return is late

Additionally, you need to be aware of any changes in the tax code that could affect your startup. There was a big change enacted last year (Section 174) this past tax season that changes the way you can expense US & International R&D expenses.

Section 174 is a new part of the tax code effective beginning with tax year 2022. It changes the way profits are calculated for your corporate taxes.

This ruling will have an impact on all startups. It will especially impact startups that have started to generate revenue (especially global startups).

Essentially, it can make it so startups with revenue and no actual profits, owe a significant amount in taxes.

This is because Section 174 requires that R&D expenses are not immediately deducted but are spread out over a period of time (5 years for US; 15 years for International).

Fondo can file your Federal Tax Extension (avoid $10,000+ in penalties) and provide you with a Startup Tax Plan outlining your obligations -- all for $1 when you sign up by Friday at 6pm PST: tryfondo.com/1

There are a lot of deadlines and requirements for tax season, but don't let that intimidate you. Simply being aware of the deadlines and what's required will put you ahead of most startups.

Fondo is an all-in-one accounting platform with financial experts to get your bookkeeping done, taxes filed, and cash back from the IRS. We’d love to take all of this off your plate! We are always here to assist you.

This guide for informational purposes only and does not constitute legal or tax advice or create an attorney-client relationship. Companies should consult their own attorneys or tax accountants for advice on these issues. Because of the generality of the issues discussed in this piece, the information provided may not apply in all situations and should not be acted upon without specific legal or tax advice based on particular situations.